Navigating the world of health insurance can feel like deciphering a complex puzzle. With terms like deductibles, copays, and coinsurance floating around, it’s easy to feel overwhelmed. But fear not! In this article, we’ll break down the essential differences between deductible vs copay, helping you grasp the implications of these terms on your financial health. By the end, you’ll have a clearer picture of how these costs work together, empowering you to choose a health insurance plan that meets your needs while keeping your wallet in check. Let’s dive in and simplify the seemingly complicated landscape of health insurance expenses!

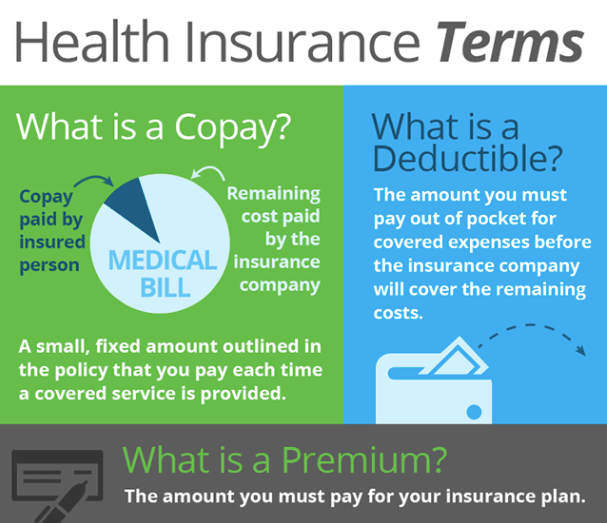

What is Copay?

Both the insurer and insured share the expenses of medical treatment when an insurance policy has a copay clause. Further, the clause may include a condition of a fixed amount or fixed percentage. The policyholder must give the fixed amount or percentage, while the insurer pays the remaining amount.

Example of Fixed Amount and Fixed Percentage Copay

In a fixed amount clause, the policyholder pays a fixed amount, say USD 5000, irrespective of the total treatment cost. The insurer will cover the rest of your medical treatment.

In a percentage clause, the policyholder has to pay in percentage of the total treatment cost. Say 15% is the agreed amount, and USD 10,000 is the total treatment expenses. In such an example, the policyholder will have to pay 1,500 USD of the total amount while the insurer will handle the remaining 8,500 USD.

What is a Deductible?

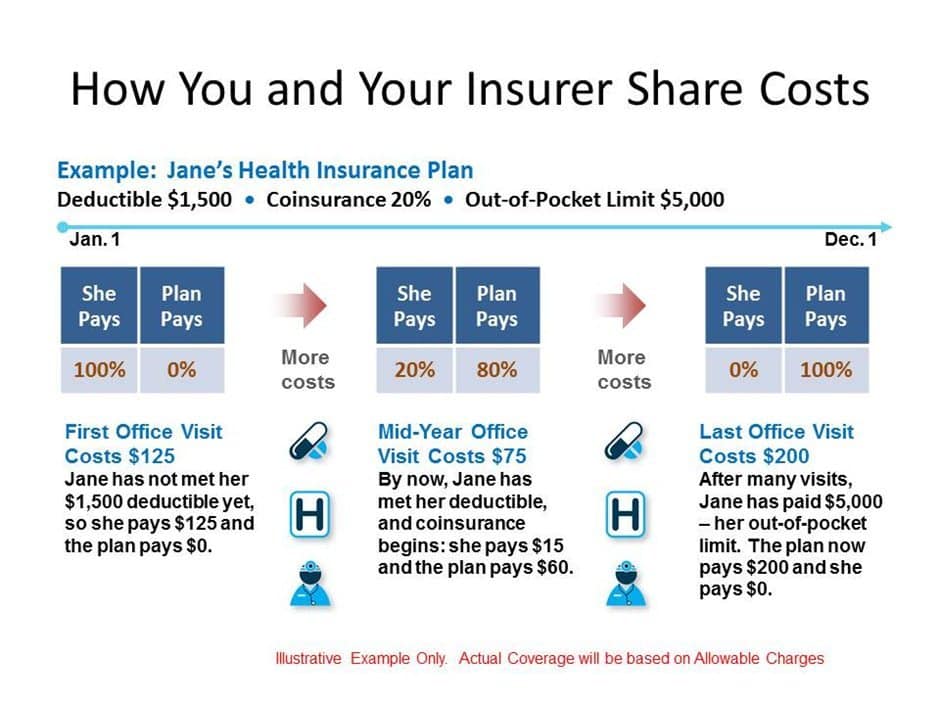

Consider deductible a flat fee levied each year on most eligible medical services or medications. You have to pay the amount upfront, post which your insurance plan will contribute to your medical expenses. Deductibles can be an annual contribution or may vary for each treatment.

Note: If you have a high-deductible health plan, you may be eligible to set aside money in a tax-advantaged Health Savings Account.

Example of a Deductible

If you have a deductibles clause stating an amount of USD 3,000, you will have to pay it upfront. The company will only activate the health insurance policy after you pay USD 3,000 toward deductibles per the clause.

What is Coinsurance?

Coinsurance is the percentage of medical treatment expenses you would incur after you pay the deductibles. It is usually defined as a fixed percentage or amount, called coinsurance after deductible. Coinsurance is identical to the copayment clause under health insurance.

Coinsurance Example

If the coinsurance clause in your insurance policy states a 10% fixed percentage, you’ll bear 10% of the treatment expenses. The insurance company will cover the remaining 90% of the total expenses. However, the company calculates this amount after you pay your deductibles, referred to as coinsurance after deductible.

Note: Always check for the list of the covered services. If some of your expenses are not eligible for cover under the policy, you have to pay the entire bill yourself, otherwise known as 100 coinsurance.

What is an Insurance Premium?

A health insurance premium is the recurring payments you make to manage your health insurance plan. Mostly, you pay a health insurance premium at a monthly or biweekly interval and it may include a high-deductible. As an employee, the healthcare premium would be deducted from your paycheck.

Features of Out-of-the-Pocket Health Insurance Expenses

Are you wondering, “how does health insurance deductible work?” To illustrate how copay and coinsurance works, we have compiled the features for you.

Copay

Here are the features of copay that you need to understand.

- The feature is popular in metropolitan cities where the average cost of treatment and the disposable income of individuals are higher.

- Because the average treatment cost for senior citizens is higher, this clause is more popular in insurance policies.

- The health insurance premium is higher when the fixed copayment component is lower.

- With copayment features, the insurer covers most of the treatment cost. Here, the policyholder only has to bear the fixed amount. If there’s no copayment feature/clause in the insurance policy, the entire treatment expense will be borne by the insurer.

Deductible

Let us now move on to deductibles and understand their features.

- Deductibles help in reducing the number of healthcare premium payments toward health insurance policies.

- However, it might lead to a rise in the total cost incurred by the policyholder toward their treatment.

- It is usually levied on policyholders to guard insurance provider’s against unnecessary claims.

Coinsurance

Let us run through the features of coinsurance for a better picture of health insurance in the United States.

- Like with deductibles, the coinsurance plan will only come into play when the policyholder pays the deductible amount. It is called coinsurance after deductible.

- It protects policyholders against claims, especially larger ones.

- The coinsurance percentage provided by the insurance company remains fixed.

Deductible vs Copay

Check the different parameters below to gauge the difference between deductible and copay.

Deductible vs Copay: Applicability

Copay: The health insurance policyholders must pay a fixed amount or a fixed percentage of their total medical treatment costs. Besides, the insurance provider/company will cover the rest of the sum. Moreover, the copay clause says that the policyholder and the insurer will share the expenses incurred.

Deductible: It is what policyholders have to pay before their policy starts contributing to their medical expenses. Further, it is usually a fixed amount of money that the clause states. The insurance provider decides on the amount. They also determine whether the clause is applicable on a per-treatment or per-year basis.

Deductible vs Copay: Impact on Premium

Copay: When the copay amount is higher, the policyholder is liable to pay smaller premium amounts.

Deductible: Deductibles usually allow the insurance policyholders to pay smaller premiums.

Deductible vs Copay: Impact of Coinsurance Clauses

Copay: Insurance providers often use Copay and coinsurance clauses interchangeably.

Deductibles: When a coinsurance clause is added, policyholders have to pay the coinsurance after the deductible amount. The payment is on top of deductibles as part of the clause.

Deductible vs Copay: Implementation

Copay: Copay does not apply to all healthcare services. It only applies to specific ones.

Deductibles: It is implemented before the insurance policy starts. Therefore, to avail of the insurance, it is mandatory to pay the deductibles.

What is Coinsurance vs Copay?

We have been through all three cost-sharing terms of health insurance and deductible vs copay. It brings us to the next big question if you wish to know about the terms in depth. What is the difference between copay and coinsurance or coinsurance vs copay?

Applicability

Copay: The health insurance policyholders must pay either the fixed amounts or fixed percentages of their total medical costs. The insurer covers the rest. The copay clause says that the policyholder and the insurer will share the expenses incurred.

Coinsurance: Coinsurance is generally associated with deductibles with a payment structure similar to copayment. It is the percentage of medical treatment expenses you have to contribute after the payment of deductibles. Usually paid in the percentage form, it remains fixed and in line with the coinsurance clause.

Payment Process

Copay: Every time you take any medical service, you’ll have to make your portion of payments based on the copay clause.

Coinsurance: After paying your deductibles, coinsurance comes into the picture. You are liable to pay for this to avail of a medical insurance cover.

Payment Intervals

Copay: You have to make the payment while availing of the medical service/treatment.

Coinsurance: Your insurance provider will bill your due amount from the payment. You have to make the payment directly to your insurer.

Relationship with Deductibles

Copay: Payment of deductible with copay is not mandatory. Further, the copay clause counts toward the deductibles only in some cases and under specific circumstances.

Coinsurance: Concerning the coinsurance clause, the coinsurance after deductible amount is only paid after paying the deductible.

Deductible vs Coinsurance

Let us also see through the difference between deductible and coinsure to see the bigger picture.

Applicability

Coinsurance: It is the percentage of medical treatment expenses you would incur after you pay the deductibles. Further, coinsurance after deductibles is defined as a fixed percentage.

Deductible: It is what policyholders have to pay before their policy starts contributing to their medical expenses. Deductibles are usually a fixed amount of money that the clause states. The insurance provider decides on the amount, and whether the clause is applicable on a per-treatment or per-year basis.

Limitation in Payments

Coinsurance: Each time you claim for insurance, you are liable to pay coinsurance as the policyholder.

Deductible: Once you have paid the mandatory deductible amount for one year, the payment toward that year ends. It is a yearly payment.

Variability in Payment Amounts

Coinsurance: The payment amount toward coinsurance depends on the treatment expense since it is a percentage of the total costs incurred.

Deductible: Deductibles are fixed yearly payments and do not depend on the treatment costs whatsoever.

Various Risk Factors

Coinsurance: Coinsurance is directly proportional to the total treatment cost incurred (a percentage of total expense). Therefore, when the cost of medical treatment is high, the out-of-pocket expenditure will be too.

Deductible: There is no significant risk in the case of deductibles. Deductibles are fixed amounts that are not in sync with the total cost of expenses.

What is Out-of-Pocket Maximum?

Let us now analyze deductible vs out of pocket. The deductible is the maximum amount the policyholder has to pay for their covered medical costs in a particular year. The maximum amount includes all the money spent toward deductibles, coinsurance, and copays.

Once policyholders reach their out-of-pocket maximum in a year, their health plan will cover the remaining medical and prescription costs. However, note that the health insurance premiums don’t count here.

Out of Network vs In-Network Providers

Some health insurance plans have two sets of clauses (deductibles, copays, coinsurance, out-of-pocket maximums), one for each provider. These are in-network and out-of-network.

Usually, in-network providers are cheaper compared to out-of-network providers. It is because the insurance company negotiates and brokers deals with the doctors and hospitals in the network.

The in-network provider can be anywhere and not necessarily near where you live. Ensure you choose to go with in-network providers for availing most of your services. It is beneficial as they are cheaper and also make more fiscal sense.

FAQs

What Does ‘0 Coinsurance’ Mean?

Contrary to 100% coinsurance, ‘0 coinsurance’ means you do not have to pay any part of the health care cost. It indicates that you have no out-of-the-pocket payment obligation. Further, it includes coinsurance after deductible, or the obligation to pay deductible always applies.

What Does 20 Coinsurance Mean?

A 20 coinsurance is all about the math, as it means you are responsible for 20% of your medical bill. It indicates that you shall contribute 20% of the total amount: USD 2000 for USD 10000 worth of treatment received.

What Is An Annual Deductible?

The annual deductible is the mandatory amount you need to pay before your policy starts to contribute. Furthermore, imagine you need to analyze deductible vs premium. Here, a premium is a recurring payment you make to maintain the insurance policy. Contrarily, a deductible is a once-in-a-year payment that you make before your insurance policy starts providing.

What Is Coinsurance After Deductible?

A coinsurance policy pays after you pay the deductible amount. Generally, deductible works with coinsurance. Hence, it is referred to as coinsurance after deductible.

Deductible vs Copay: The Final Answer

While knowing the terms is critical, it is also crucial to understand that they are not mandatory in every policy. If you catch sight of policies with copayment, coinsurance, and deductible clauses, you are able to understand how they bring down the premium. This means that you agreed to pay a small recurring amount, only to pay quite a bit out of pocket in the future.

A possible decision would be to choose policies that do not include cost-sharing clauses. While they will spare you the hassle of situations where you don’t have the money for co-pays and need urgent treatment, they can be a quite expensive upfront.

Whatever be the case, it is sensible to set aside time and money for the health insurance needs for you and your family.